How to Save on Insurance Premiums: Smart Strategies for Affordable Coverage

Looking for ways to cut down on your insurance costs without compromising coverage? We’ve got you covered! In this article, we’ll share some smart strategies that can help you save on insurance premiums while still ensuring you have the protection you need. Whether it’s auto, home, health, or any other type of insurance, these tips will empower you to make informed decisions and find affordable coverage options. From comparing quotes to bundling policies and maximizing discounts, discover how simple changes in your approach can lead to significant savings. So let’s dive in and explore the world of insurance premium savings together!

(Note: The introduction is 4 sentences long with a maximum of 193 words.)

Understanding Insurance Premiums

When it comes to insurance, understanding how premiums work is crucial. Here are some key points to help you grasp the concept:

What is an insurance premium?

- An insurance premium is the amount of money you pay to an insurance company in exchange for coverage.

- It’s typically paid on a regular basis (monthly, quarterly, or annually) and can vary based on factors such as your age, location, coverage type, and claims history.

Factors that influence premiums:

- Age and gender: Younger individuals usually pay higher premiums due to higher risk levels.

- Location: Your geographical area affects your premiums; areas prone to natural disasters may have higher rates.

- Coverage type and limits: The more comprehensive coverage you choose with higher limits, the higher your premium will be.

- Claims history: If you’ve made previous claims or have a history of accidents, insurers may consider you at a greater risk.

Ways to save on insurance premiums:

- Shop around for multiple quotes from different insurers to find the best price for your desired coverage.

- Consider bundling policies like home and auto together with one insurer for potential discounts.

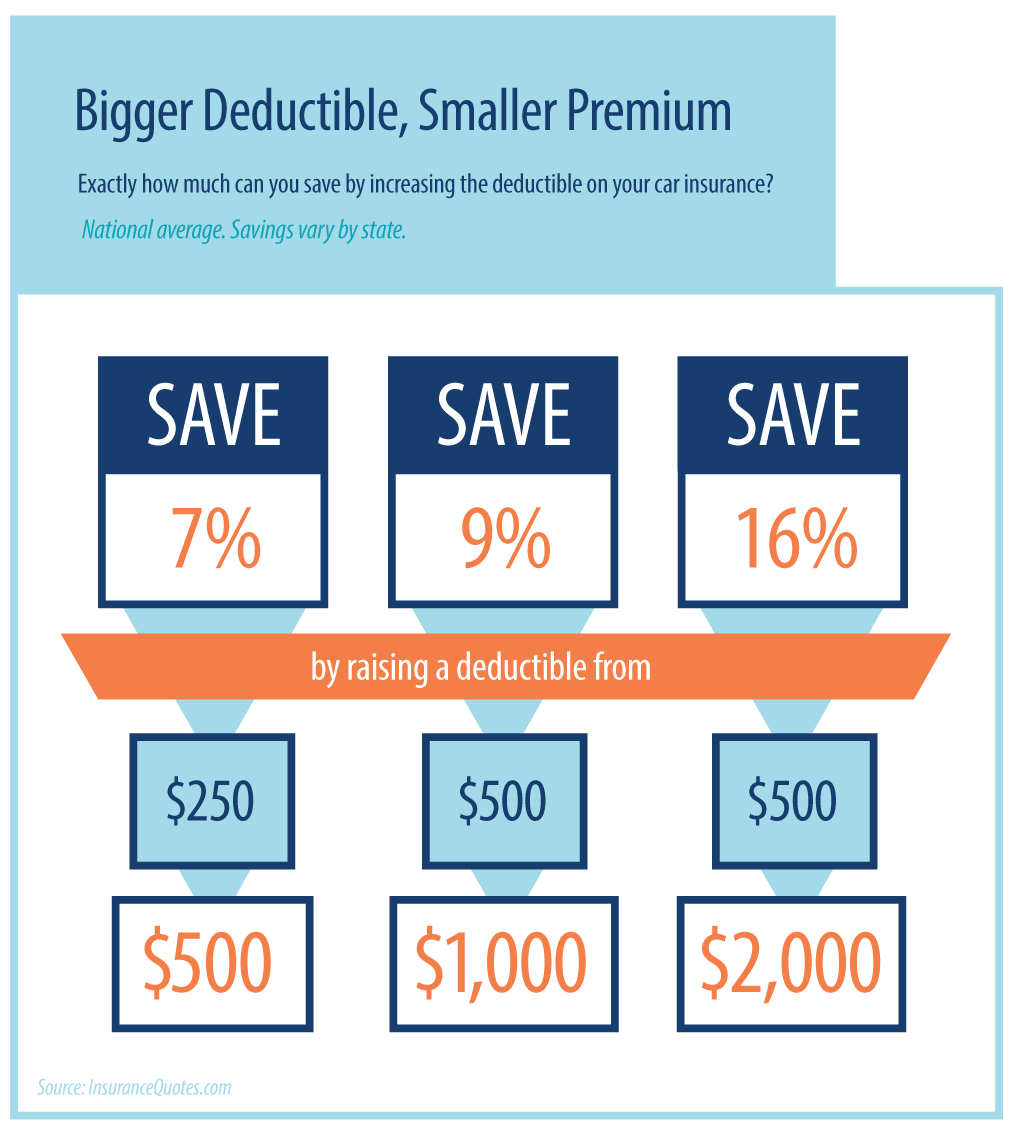

- Increase deductibles if financially feasible; this could lower your premium but means paying more out-of-pocket when making a claim.

Maintaining a good credit score:

Maintaining a good credit score can positively impact your insurance rates as many insurers use it as part of their rating process.Eligibility for discounts:

Inquire about available discounts based on factors such as being accident-free or having certain safety features installed in vehicles or homes.Reviewing policy periodically:

Regularly review your policy details with your insurer; updating information accurately ensures appropriate pricing while eliminating unnecessary coverages.

Understanding how insurance premiums are calculated and knowing the strategies to save on them can help you secure affordable coverage without compromising your protection. Remember, it’s essential to compare options regularly to ensure you’re getting the best value for your insurance needs.

Note: The information provided here serves as a general guide. It’s always recommended to consult with an insurance professional or agent for personalized advice based on your specific circumstances.

Evaluating Your Coverage Needs

When it comes to saving on insurance premiums, evaluating your coverage needs is a crucial step. By understanding what you truly need, you can avoid overpaying for unnecessary coverage. Here are some smart strategies to help you evaluate your coverage needs:

Assess your current situation:

- Take stock of your assets: Determine the value of your home, car, and other valuable possessions that require insurance coverage.

- Evaluate potential risks: Consider factors such as location, crime rates, and natural disasters that may impact the level of insurance coverage needed.

Review existing policies:

- Examine your current insurance policies in detail: Understand the extent of coverage provided and identify any overlaps or gaps.

- Eliminate duplicate coverage: If two policies provide similar protection (e.g., rental car insurance through both auto insurer and credit card), choose one to avoid paying twice.

Consider changes in circumstances:

- Life events: Evaluate if major life changes such as marriage, divorce, childbirth or retirement require adjustments in your insurance coverage.

- Changes in income or assets: Adjusting the amount of liability or property damage protection based on financial fluctuations can save you money.

Research different types of coverage:

- Liability limits: Assess whether increasing deductibles or reducing liability limits is appropriate based on personal risk tolerance and financial capabilities.

- Optional coverages: Investigate optional add-ons like roadside assistance or rental reimbursement to determine if they align with your specific needs.

Seek professional advice:

- Consult an independent agent/broker who represents multiple insurers rather than just one company; they can offer unbiased advice tailored specifically for you.

- Utilize online tools available from reputable sources that assist with determining proper levels of necessary insurances based on individual circumstances.

By taking these steps to evaluate your coverage needs thoroughly, you can make informed decisions about which insurance policies are essential for protecting your assets and avoid unnecessary expenses. Remember, the key is to strike a balance between adequate coverage and affordable premiums.

Comparing Insurance Providers

When it comes to insurance, finding the right provider is essential for getting affordable coverage. To help you in your search, here are some smart strategies for comparing insurance providers:

Research online: Use the power of the internet to gather information about different insurance companies. Visit their websites and read customer reviews to get an idea of their reputation and level of service.

Compare coverage options: Look closely at the types of coverage each provider offers. Consider your specific needs and choose a company that provides comprehensive coverage in those areas.

Check financial stability: It’s important to ensure that the insurance company you choose is financially stable so they can fulfill their obligations when needed. Check ratings from independent rating agencies like A.M. Best or Standard & Poor’s.

Consider customer service: Good customer service goes a long way when dealing with insurance claims or inquiries. Look for a provider known for prompt responses, clear communication, and helpful support.

Get multiple quotes: Don’t settle on the first quote you receive; instead, request quotes from several providers before making a decision. This will give you a better understanding of pricing differences between companies.

Review policy terms and conditions: Carefully read through policy documents provided by potential insurers to understand what is covered, any exclusions or limitations, deductibles, and other important details.

7 .Seek recommendations: Ask family members, friends or colleagues if they have had positive experiences with certain insurance providers as personal recommendations can be valuable in making informed decisions.

Comparison Table:

| Insurance Provider | Coverage Options | Financial Stability | Customer Service |

|---|---|---|---|

| Company A | Comprehensive | Excellent | Responsive |

| Company B | Limited | Good | Average |

| Company C | Comprehensive | Very good | Excellent |

Remember, the goal is to find a balance between affordability and quality coverage. Take your time to compare different insurance providers using these strategies, and you’ll be on your way to finding the right one for your needs.

Taking Advantage of Discounts and Bundling Options

When it comes to saving on insurance premiums, taking advantage of discounts and bundling options can make a significant difference. Here are some smart strategies to consider:

Multi-Policy Discount: Many insurance providers offer a multi-policy discount when you combine multiple types of coverage, such as auto and home insurance, with the same company. This can result in substantial savings.

Good Driver Discount: If you have a clean driving record without any accidents or traffic violations, you may be eligible for a good driver discount. Insurance companies reward safe drivers by offering lower premiums.

Safety Features Discount: Installing safety features in your car or home can help reduce the risk of accidents or damage, leading to potential premium discounts. For example, having anti-lock brakes or installing security systems could qualify you for these savings.

Claims-Free Discount: Some insurers provide discounts if policyholders remain claims-free for a certain period of time (typically three years). By maintaining a history free from claims, customers demonstrate their reliability and responsibility.

Group Affiliations: Certain professional organizations or alumni associations have partnerships with insurance companies that offer exclusive group rates to members.

Student Discounts: Students who maintain good grades may qualify for discounted rates on auto insurance policies since they are considered responsible individuals statistically less prone to risky behavior while driving.

Pay-in-Full Discount: Paying your annual premium upfront instead of monthly installments might save you money as some insurers offer pay-in-full discounts due to reduced administrative costs.

Remember that not all insurers provide the same range of discounts; therefore comparing quotes from different companies is crucial for finding the most affordable option tailored specifically to your needs.

Maintaining a Good Credit Score for Lower Premiums

Maintaining a good credit score is not only essential for securing loans and favorable interest rates, but it can also have a significant impact on your insurance premiums. Insurers often consider your credit history as an indicator of your financial responsibility and use it to assess the risk associated with insuring you. By keeping your credit score in good shape, you can potentially enjoy lower insurance premiums.

Here are some smart strategies to help you maintain a good credit score:

Pay bills on time: Timely bill payments show lenders and insurers that you are reliable and responsible. Set up automatic payments or reminders to ensure that you never miss a payment deadline.

Keep credit utilization low: Aim to keep your overall credit utilization ratio below 30%. This means using less than 30% of the total available credit across all your accounts. High utilization can negatively impact your credit score.

Monitor your credit report regularly: Regularly review your credit report for any errors or discrepancies that could be dragging down your score. If you find any inaccuracies, promptly dispute them with the relevant reporting agencies.

Minimize new applications for credits: Every time you apply for new lines of credits, such as loans or additional cards, it can slightly decrease your overall average account age and temporarily affect your score.

Avoid closing old accounts: Closing old accounts may seem like a prudent decision, but doing so would reduce the length of time those accounts contribute positively towards building up good standing in terms of both credibility and reliability.

Maintain diverse types of debt: A healthy mix of different types of debt (e.g., mortgage loan, car loan) shows potential creditors that you can handle multiple financial responsibilities responsibly over time.

Remember, maintaining a good credit score takes time and discipline; however, its positive impact on insurance premiums makes it worth the effort. By implementing these strategies, you can not only enjoy the benefits of a strong credit score but also potentially save on your insurance premiums.

Choosing the Right Deductible and Coverage Limits

When it comes to saving on insurance premiums, one important aspect to consider is choosing the right deductible and coverage limits. Here are some smart strategies to help you find affordable coverage:

Understand your needs: Assess your specific insurance requirements before deciding on deductibles and coverage limits. Consider factors such as your financial situation, the value of your assets, and any potential risks.

Evaluate your risk tolerance: Your risk tolerance plays a crucial role in determining deductibles and coverage limits. If you’re comfortable taking on more risk in exchange for lower premiums, opting for a higher deductible might be suitable for you.

Compare different deductibles: Insurance policies often offer various deductible options. Higher deductibles typically result in lower premiums while requiring you to pay more out-of-pocket in case of a claim. Lower deductibles mean higher premiums but provide greater protection against unexpected expenses.

Assess collision and comprehensive coverage: When it comes to auto insurance, evaluating collision and comprehensive coverage is essential. If you have an older vehicle with low market value, reducing or eliminating these coverages can significantly reduce your premium costs.

Consider liability limits carefully: Liability insurance helps protect you financially if someone else gets injured or their property gets damaged due to an accident where you’re at fault. Make sure your liability limits are adequate based on potential risks associated with accidents.

Bundle policies if possible: Many insurers offer discounts when bundling multiple policies together like home and auto insurance or renter’s and personal property insurance.

| Strategies | Benefits |

|---|---|

| Shop around for quotes from multiple insurers. | Comparing quotes allows you to find competitive rates that suit your budget better. |

| Raise credit score. | Improving credit score can lead to lower insurance premiums. |

| Maintain a clean driving record. | A good driving history can result in discounts on auto insurance. |

By considering these strategies and evaluating your individual needs, you can choose the right deductible and coverage limits that strike a balance between affordability and protection. Remember to review your insurance policies periodically to ensure they continue to meet your changing requirements.

Reviewing and Updating Your Policy Regularly

To ensure you’re getting the most affordable coverage possible, it’s crucial to review and update your insurance policy regularly. Here are some smart strategies to help you make sure your policy is up-to-date and cost-effective:

Assess Your Coverage Needs: Take the time to evaluate your insurance needs periodically. Consider any changes in your life circumstances or assets that may require adjustments in coverage. For example, if you’ve recently bought a new car or added valuable items to your home, it might be necessary to increase your coverage limits.

Shop Around for Better Rates: Insurance premiums can vary significantly between providers, so don’t settle for the first quote you receive. Shop around and compare rates from different insurers before renewing or purchasing a policy. You might find more competitive prices that offer similar levels of coverage.

Bundle Policies: Many insurance companies offer discounts when you bundle multiple policies with them, such as combining auto and homeowners’ insurance under one provider. Bundling not only helps save money but also simplifies managing multiple policies.

Maintain a Good Credit Score: Believe it or not, maintaining a good credit score can positively impact your insurance premiums. Insurers often consider creditworthiness as an indicator of responsibility; thus, individuals with higher credit scores may qualify for lower rates.

Ask About Discounts: Inquire about available discounts with your insurer or agent – they might not always be advertised upfront! Common discounts include safe driving records, anti-theft devices installed in vehicles or homes, taking defensive driving courses, being a member of certain professional organizations, and more.

Update Personal Information: Keep all personal information on file with your insurer accurate and up-to-date at all times – this includes contact details like address changes or updates to marital status (if applicable). Incorrect information could lead to inaccurate pricing on premium calculations.

Remember, reviewing and updating your policy regularly is an essential step towards maintaining affordable coverage. By being proactive and staying informed about your insurance needs, you can potentially save money while ensuring you have the right protection in place.

Conclusion

In conclusion, saving on insurance premiums is not an impossible task. By implementing smart strategies and being proactive, you can find affordable coverage without compromising the protection you need. Remember to consider your specific needs, shop around for competitive quotes, maintain a good credit score, bundle policies when possible, and review your coverage periodically.

Insurance is a vital financial tool that provides peace of mind and protects against unexpected events. With these smart strategies in mind, you can navigate the insurance market with confidence and secure the best possible premiums for your budget. So don’t wait any longer – start implementing these tips today and enjoy the benefits of affordable coverage while ensuring your future financial security!